In today’s fast-paced financial environment, having access to credit is essential, even for individuals with limited or poor credit history. No credit check credit cards provide instant approval and quick access to funds, helping users manage purchases and rebuild their credit profile. This guide explores the benefits, risks, and practical steps for obtaining these cards.

Understanding No Credit Check Cards: Benefits and Risks

If you’re concerned about your credit history but need access to credit, no credit check credit cards can be an option. These cards often bypass traditional credit evaluations, focusing instead on other criteria such as income, employment status, and age. While they offer financial flexibility, it’s important to be aware of potential downsides.

1. Exploring No Credit Check Options

No credit check credit cards are particularly useful for those who have been denied conventional credit cards. Approval is usually based on factors other than your credit score, including:

- Proof of income or employment

- Bank account verification

- Age and residency requirements

However, these cards often come with fees, deposit requirements, and higher interest rates, so careful selection is crucial. Look for cards with manageable costs that align with your financial situation.

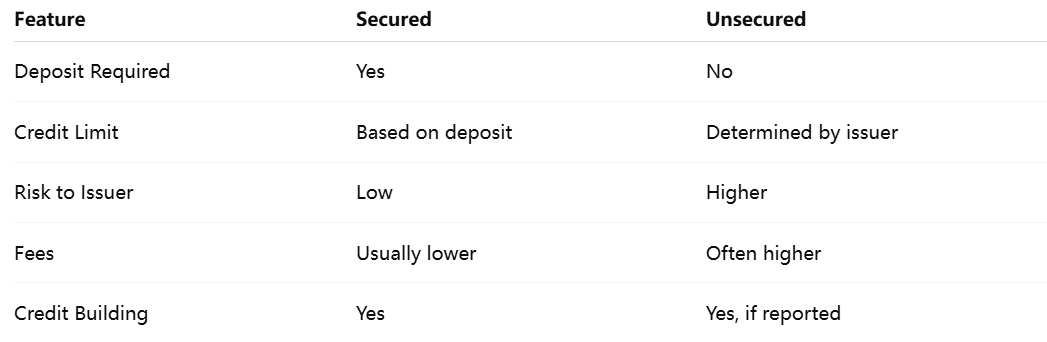

2. Secured vs. Unsecured Cards

When searching for no credit check options, you’ll encounter both secured and unsecured cards.

- Secured Cards: Require a security deposit that typically acts as your credit limit. They are lower risk for the issuer and help you build or rebuild credit over time.

- Unsecured Cards: Don’t require a deposit, but may carry higher fees or interest rates. Approval often depends on income or financial stability.

Both types can be effective tools for rebuilding credit, but secured cards usually present a lower initial financial risk.

3. Instant Access and Approval

Some credit card issuers provide instant access to your card number upon approval, which allows you to:

- Make online purchases immediately

- Use mobile payment apps before receiving the physical card

- Quickly manage urgent expenses

This feature is especially helpful for individuals needing immediate credit access while waiting for the physical card.

4. Building or Rebuilding Credit

Using a secured card responsibly can positively impact your credit score. Key practices include:

- Making timely payments

- Keeping balances low

- Monitoring credit reports regularly

For those with poor or no credit history, no credit check cards that report to credit bureaus can serve as stepping stones to mainstream credit products.

How to Secure a Credit Card Instantly Without Traditional Checks

Even without a strong credit history, you can still gain access to credit by following these strategies:

1. Understand No Credit Check Options

Identify cards that prioritize income verification or other non-credit-based factors. This approach increases your likelihood of approval without a traditional credit inquiry.

2. Consider Secured Cards First

Secured cards are often the most accessible, requiring a refundable security deposit that doubles as your credit limit. Responsible usage can help establish or repair your credit.

3. Look for Credit-Building Features

Choose cards that report activity to major credit bureaus and offer tools like payment reminders or credit monitoring to guide responsible financial management.

4. Instant Use After Approval

Some issuers allow you to access your card number instantly, enabling immediate online or mobile purchases. Confirm this feature before applying if urgent credit access is needed.

From Application to Approval: Quick Online Processing

Understanding the nuances of online credit card applications can increase your chances of success:

- Instant Approval vs. Instant Use: Instant approval means your application is accepted quickly; instant use allows you to spend using the card number immediately.

- Approval Rates: Secured cards generally have higher approval rates due to reduced risk, while unsecured options may have stricter criteria.

- Prequalification: Many issuers offer prequalification using soft credit checks to gauge approval odds without affecting your credit score.

Choosing Between Secured and Unsecured Options

- Secured Credit Cards: Require a deposit, ideal for cautious credit rebuilding.

- Unsecured Credit Cards: Offer convenience without a deposit, but may involve higher fees or stricter approval standards.

Other considerations:

- Annual fees and interest rates

- Rewards programs or cash-back opportunities

- Credit-building tools provided by the issuer

Carefully evaluating these factors will help you select the card best suited to your needs.

Q&A

Q1: What is the difference between secured and unsecured no-credit-check cards?

A1: Secured cards require a deposit, often equal to the credit limit, reducing risk for both parties. Unsecured cards don’t require a deposit but may have higher fees or stricter approval criteria.

Q2: What is the difference between instant approval and instant use?

A2: Instant approval means your application is accepted quickly. Instant use means you can start spending immediately using the card number, even before the physical card arrives.

References

- Bankrate – Best Credit Cards for Bad Credit

- NerdWallet – Instant Credit Card Numbers

- LendingTree – No Credit Check Cards